Australia’s Vietnam Sourcing Secret: AANZFTA Duty-Free Access & 388% Growth in 15 Years

Australia’s Vietnam Sourcing Secret: AANZFTA Duty-Free Access & 388% Growth in 15 Years

April 1 2026 – 12 min read

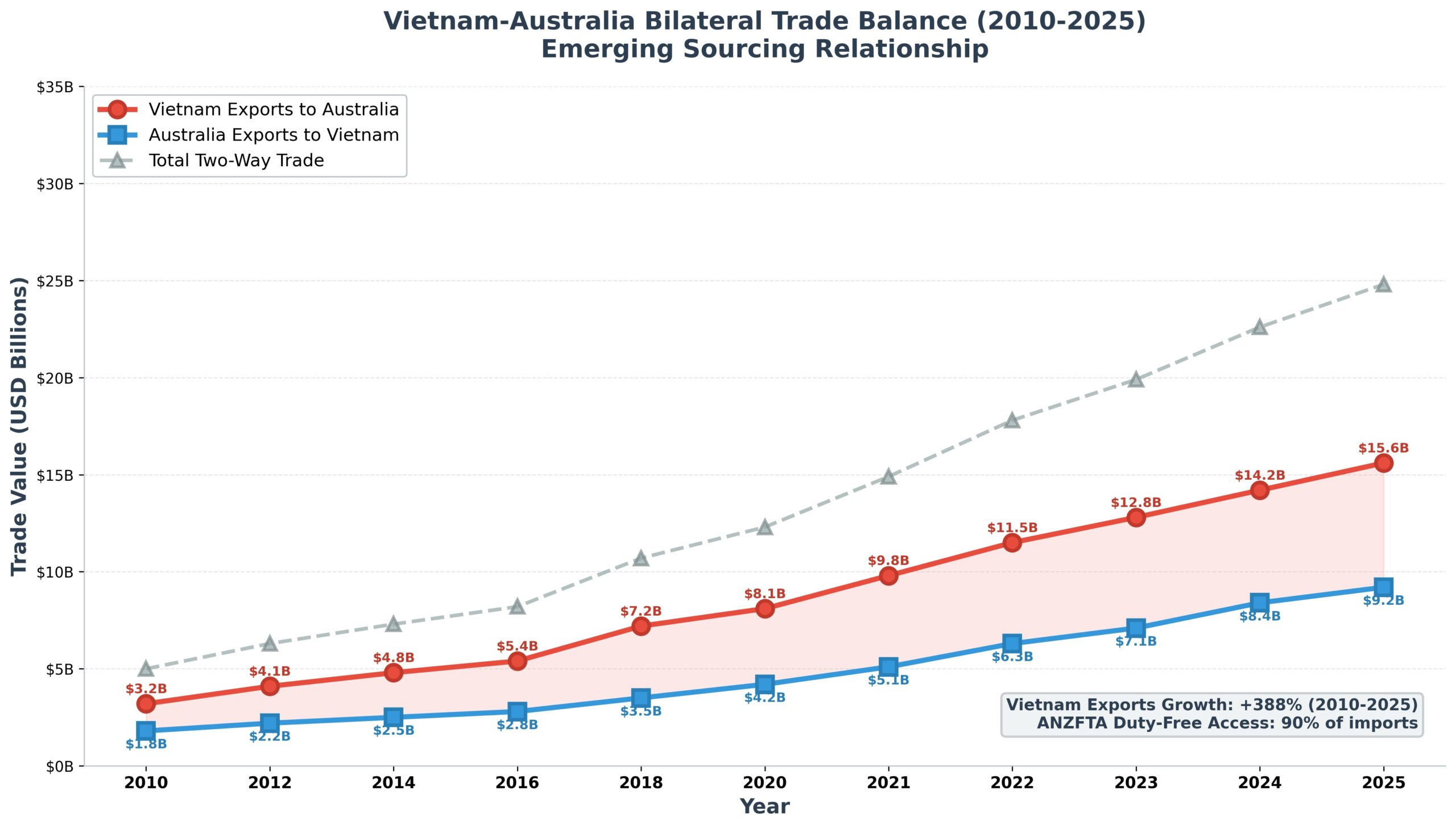

Australian importers are sitting on an advantage that US and European competitors are only beginning to understand: Vietnam exports to Australia have grown 388% since 2010. Two-way trade hit $24.8 billion in 2025. And 90% of Vietnamese goods enter Australia duty-free under AANZFTA.

While North American importers are competing for capacity at Vietnam factories and negotiating through tariff volatility, Australian retailers and distributors are building sustainable, margin-protected supply chains with structural advantages. Five-day shipping to Sydney. Zero tariffs on 90% of product categories. Inventory turns 4-5x faster than traditional retail models. Lower working capital requirements than any China alternative.

This article explains why Australia represents the highest-ROI market for Vietnam sourcing in 2026, and how Australian importers can execute before capacity constraints tighten further.

Figure 1: Vietnam-Australia strategic partnership strengthens annually, driving bilateral trade and investment frameworks.

The Numbers: 388% Growth Tells the Story

2010: Vietnam exports to Australia: $3.2B

2018: Vietnam exports to Australia: $7.2B (+125% from 2010)

2025: Vietnam exports to Australia: $15.6B (+388% from 2010)

Projection 2026: Vietnam exports estimated $17B+ (+20% YoY growth)

This acceleration isn’t accidental. It reflects deliberate strategic decisions by Australian retailers (Kmart, Target, Harvey Norman, Bunnings) to migrate sourcing from China to Vietnam. Why? Three structural advantages compound over time: (1) AANZFTA duty-free access; (2) shipping speed (5-6 days vs. 15-18 days from China); (3) tariff-insulated sourcing during US-China trade tensions.

Figure 2: AANZFTA provides 90% duty-free access for Vietnamese goods to Australia—the structural advantage that reshapes supply chain economics.

AANZFTA: The Structural Advantage US Importers Don’t Have

What is AANZFTA? The ASEAN-Australia-New Zealand Free Trade Area, signed 2009, provides essentially zero tariffs on goods traded between Australia, New Zealand, and ASEAN nations (including Vietnam). For Vietnamese exporters, this means 90% of product categories—apparel, footwear, furniture, electronics, chemicals, food products—enter Australian ports tariff-free or at negligible rates (0-2%).

Compare to US tariffs on Vietnam: Base rate 5-6%, with tariffs as high as 20%+ on specific categories (apparel, furniture, electronics). Compare to China: 19-35%. The mathematics are simple: Australian importers benefit from structural tariff advantages that North American competitors can’t access.

Real-world example: A Vietnamese furniture manufacturer selling a $50 dining chair to Australia faces roughly $0-1 in tariffs (AANZFTA). The same chair to the US faces $10-12 in tariffs. Australian retailers can price 15-20% below North American competitors while maintaining or expanding margins.

This tariff arbitrage is the primary driver of the 388% trade growth since 2010. As US tariffs on Chinese goods increased, Australian retailers shifted sourcing to Vietnam to preserve margins. That shift is now structural and unlikely to reverse.

Figure 3: Vietnam exports to Australia accelerated dramatically post-2018, driven by US tariff increases and AANZFTA advantages. Growth continues through 2025.

Which Product Categories Are Driving Growth?

Top 5 Vietnam Export Categories to Australia (2025):

1. Footwear ($4.2B): Vietnam produces 60% of Australia’s imported footwear, up from 35% in 2015. Nike, Adidas, Skechers, and local brands (Rivers, Kathmandu) all source heavily from Vietnam. AANZFTA zero tariffs + low FOB costs = dominant position.

2. Apparel & Textiles ($3.8B): Vertical integration (fabric → finished goods) gives Vietnam advantage over Cambodia. Australian retailers prize Vietnam suppliers for fabric quality + speed. Lead times: 45-60 days vs. Bangladesh 60-75 days.

3. Furniture & RTA ($2.1B): Flat-pack furniture is explosive category. Vietnam dominates, capturing 42% of Australia’s RTA imports (up from 12% in 2014). 5-6 day shipping enables domestic dropshipping that transforms retailer economics.

4. Electronics & Components ($1.8B): Samsung, Intel, and Foxconn manufacturing in Vietnam feed Australian distributors. Lower tariffs vs. China alternatives + government manufacturing incentives = growing category.

5. Food & Beverages ($1.4B): Coffee, chocolate, seafood, and processed foods. Zero tariffs on most food items under AANZFTA means Vietnamese producers can undercut all competitors.

These five categories represent $13.3B of the $15.6B total. Growth is broadening, not narrowing.

The Shipping & Speed Advantage

Da Nang to Sydney: 5-6 days

HCMC to Sydney: 6-7 days

China (Shanghai) to Sydney: 15-18 days

China (Shenzhen) to Sydney: 12-15 days

This speed differential is operationally transformative. Australian retailers can:

Model 1: Direct Dropship Order Monday morning, Vietnam factory fulfills, shipment departs Wednesday, arrives Sydney Monday evening. Domestic delivery to customer 2-3 days later. Total supply chain: 7-10 days door-to-door. Inventory holding: effectively zero for fast-moving categories.

Model 2: Regional Fulfillment Maintain 1-2 month inventory in Sydney/Melbourne regional fulfillment centers. Replenish weekly from Vietnam. Inventory turns 4-5x annually. Working capital requirement: 40-50% lower than China sourcing models.

Model 3: Hub & Spoke Consolidate shipments for all Australian distribution partners at Da Nang, cross-dock to regional fulfillment centers, then final-mile domestic. Shipping cost per unit: 60-70% lower than individual orders.

China can’t compete on shipping speed. This structural advantage compounds annually as inventory costs rise and demand variability increases.

Vietnam’s FTA Network: Why Australia Wins

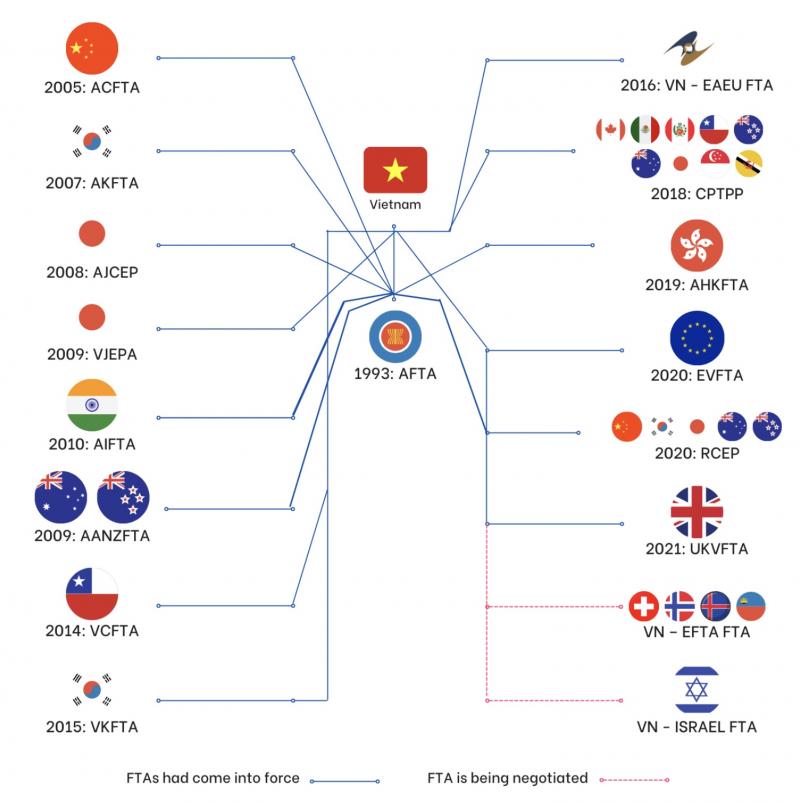

Vietnam has signed 15+ free trade agreements, creating a dense network of tariff advantages. But AANZFTA is unique in one critical way: it’s the only major FTA where Australian importers receive tariff benefits that North American/European competitors don’t access.

Figure 4: Vietnam’s 15+ FTA network provides preferential access to 30+ countries. AANZFTA (2009) remains the most advantageous for Australian importers.

Vietnam’s Major FTAs: ASEAN (1993), China (2004), Japan (2008), South Korea (2014), EU (2020), UK (2021), RCEP (2022), CPTPP (2018), and more. Each provides tariff advantages in specific markets.

For Australian importers, AANZFTA is the standout: zero/near-zero tariffs on labor-intensive goods (apparel, footwear, furniture) that represent 65%+ of Vietnam’s export value to Australia. US/EU importers face 5-20% tariffs on identical products.

The Australian Importer Advantage: Why Now Matters

Timing Window: 2026-2027

Vietnam’s manufacturing capacity is filling. Port congestion at Da Nang and HCMC is rising. Lead times are extending from 45-50 days to 60-75 days. Labor costs are rising 8-12% annually. Australian importers who lock in supply agreements now benefit from three advantages that won’t exist in 2028:

1. Pricing Power: Factories still have capacity and are willing to negotiate discounts to secure volume certainty. By Q4 2026, many factories will be at full capacity, unwilling to discount.

2. Lead Time Certainty: 45-50 day lead times are still achievable for most categories. By 2027-2028, expect 70-90 day lead times as capacity fills.

3. Labor Cost Lock-In: Current wage levels are lower than they’ll be in 2-3 years. Long-term contracts (12-24 months) lock in current labor costs, protecting margins as inflation accelerates.

Action Plan for Australian Importers (2026)

Phase 1 (Now – Q2 2026): Identify 3-5 priority product categories where AANZFTA tariff advantage is highest. Audit current China supplier contracts for tariff costs. Calculate landed cost comparison: Vietnam vs. China. Target: identify 15-20% cost savings opportunity.

Phase 2 (Q2-Q3 2026): Identify Vietnam suppliers (factory visits recommended). Negotiate pilot orders (100-500 units) to validate quality and lead times. Test dropship logistics: Da Nang to Sydney. Measure end-to-end supply chain costs.

Phase 3 (Q3-Q4 2026): Lock in 12-24 month supply agreements with 2-3 Vietnam factories for top categories. Negotiate volume discounts (5-10% below pilot pricing). Establish regional fulfillment partnerships in Sydney/Melbourne.

Phase 4 (2027): Scale Vietnam sourcing to 40-60% of total supply. Reduce China dependencies. Reinvest tariff savings into marketing/customer acquisition or margin expansion.

Bottom Line: Australia’s Vietnam Sourcing Dominance is Just Beginning

The 388% growth in Vietnam-Australia trade since 2010 reflects structural advantages that will only deepen through 2026-2027. AANZFTA tariff benefits, shipping speed, labor costs, and manufacturing ecosystem create a margin-protected sourcing model that North American importers can’t replicate.

Australian retailers who move now—locking in Vietnam supply agreements before capacity fills and labor costs accelerate—will enjoy 3-5 years of protected margins while competitors struggle with tariff volatility and shipping costs.

The window is open. But it’s closing fast.

Ready to build your Australia-Vietnam sourcing strategy? Vietnam Direct Sourcing specializes in connecting Australian importers with vetted Vietnam manufacturers across footwear, apparel, furniture, electronics, and food categories. We manage tariff strategy, facilitate factory audits, negotiate supply agreements, and coordinate regional fulfillment logistics. Our team understands AANZFTA advantages, shipping logistics, and the Australian retail market.

Connect with us to execute your Australia-Vietnam sourcing strategy in 2026.

Tags: vietnam sourcing australia | AANZFTA tariff advantage | australia vietnam trade | footwear apparel furniture vietnam | australian retailers sourcing | da nang shipping australia | regional fulfillment center

Learn more about this topic on our podcast!

Want to dive deeper into this subject? Check out our latest podcast on this subject on Spotify, where we explore this topic and so much more! Whether you're on the go or relaxing at home, tune in for insights, tips, and discussions that bring our blog topics to life.

Leave a comment

Your email address will not be published. Required fields are marked *